Despite Manufacturing surveys solid (and US factory orders surging), expectations are for the Services sector surveys today to show stagflationary signals (weak growth, surging prices).

S&P Global's Services PMI disappointedin April (final), falling from its flash print of 51.3 to 51.0, but still up from multi-year lows below 50 in March, showing justmarginal activity growth despite weak drop in sales volumes.

ISM Services PMI also disappointedin April, falling from 54.0 to 53.6 (vs 53.7 exp) amidtumbling new orders and high prices.

Under the hood it was not a pretty picture at all withnew orders slowing dramatically, Prices Paid holding near cycle highs, and employment contracting for the second month in a row...

“Although business activity returned to growth after a small decline in March,it’s clear the pace of growth has kicked down a couple of gears since the start of the year,"said Chris Williamson,Chief Business Economist at S&P Global Market Intelligence.

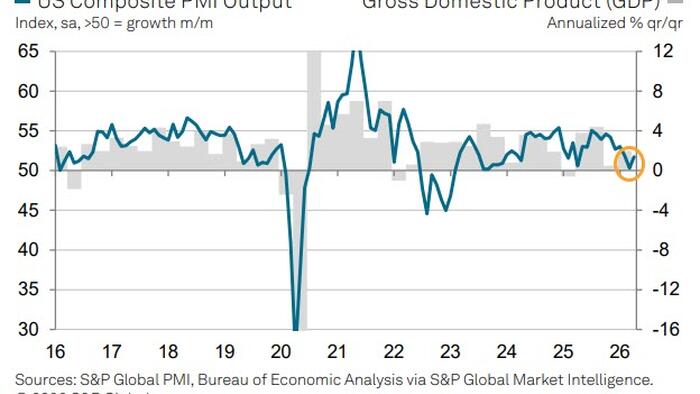

The survey data are indicative of GDP growing at a modest 1% annualized rate.

“Growth may weaken further," warns Williamson, asservice providers are reporting lower inflows of new business for the first time in two years, reflecting an intensifying hit to demand from the war in the Middle East.

“The direct impact of the war has been most evident in consumer-facing services, as high prices have led to a pull-back in discretionary spending on activities such as holidays and recreation, though transport has also been curbed by high fuel prices and travel disruptions."

However, a secondary additional driver of renewed weakness is adrop in demand for financial services, in part linked to heightened uncertainty about market outlooksbut also reflecting expectations of higher inflation and interest rates, which has hit real estate and lending activity.

But it's not just weak growth/orders, prices are surging too... broadly.

Source: ZeroHedge News