Markets are bracing for a pivotal week that could dictate the Federal Reserve's next moves on interest rates, with non-farm payrolls, consumer price index, and retail sales data set to dominate headlines. Traders and economists alike are glued to their screens, anticipating releases that might either soothe fears of a recession or ignite fresh inflation worries amid a backdrop of geopolitical tensions and uneven global growth.

The week kicks off with anticipation building toward Wednesday's CPI report, the market's preferred gauge of inflation. Economists project a headline CPI reading of 2.9% year-over-year, down slightly from last month's figure, but core CPI—stripping out volatile food and energy—is expected to hold steady at around 3.2%. Any upside surprise could reinforce hawkish bets on the Fed holding rates higher for longer, while a softer print might fuel hopes for cuts as early as June. Last month's hotter-than-expected data already prompted a reassessment of rate cut timelines, sending Treasury yields spiking and pressuring equities.

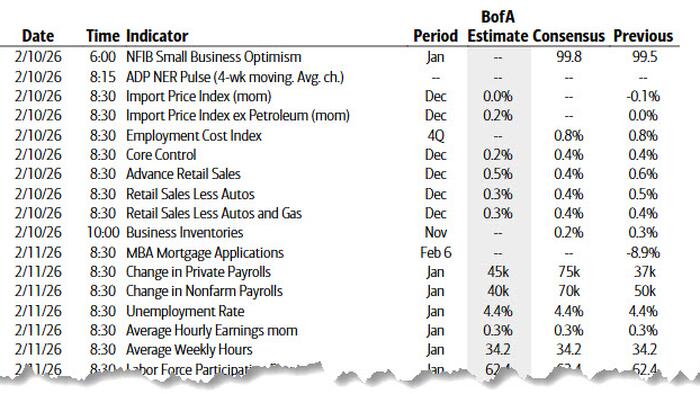

Thursday brings retail sales, a critical measure of consumer spending that drives nearly 70% of U.S. GDP. Consensus forecasts call for a modest 0.3% month-over-month gain in January figures, adjusted for seasonal factors, following December's robust performance. However, control-group sales—which exclude autos, gas, and building materials and align closely with GDP calculations—are under scrutiny. With holiday spending hangovers and rising credit card delinquencies signaling consumer fatigue, weaker-than-expected numbers could underscore cracks in household balance sheets strained by elevated borrowing costs.

Capping the week on Friday, the non-farm payrolls report will reveal January job growth, unemployment, and wage pressures. Analysts anticipate 185,000 jobs added, with unemployment ticking up to 4.1% and average hourly earnings growth cooling to 0.3% monthly. The report's revisions to prior months often steal the show—December's 333,000 gain was slashed in recent updates—highlighting data volatility. Strong payrolls might dash rate-cut dreams, boosting the dollar and yields, while tepid figures could stoke soft-landing narratives or even recession fears if revisions disappoint.

These releases arrive as the S&P 500 hovers near all-time highs, propped up by tech megacaps, yet small-cap and cyclical stocks lag, betraying underlying unease. The Fed's preferred PCE inflation gauge, due later in the month, looms large, but this week's trio could shift market pricing dramatically—currently baking in 75 basis points of cuts by year-end. Investors are also eyeing corporate earnings season wind-down and any hints from Fed speakers, in a high-stakes dance between growth resilience and persistent price pressures.

Beyond the numbers, these indicators carry broader implications for policy and politics. Robust data might embolden fiscal hawks pushing for spending restraint, while weakness could amplify calls for stimulus in an election year. As Wall Street parses every decimal, Main Street feels the real sting of affordability challenges, underscoring the high bar for the Fed to navigate without tipping into downturn.