Tomorrow marks exactly two months since the strikes on Iran began. As DB's Jim Reid writes, while there is currently a rolling, open ended ceasefire that started on 8 April, the risk of it collapsing at any point remains real. Just as the weekend news looked like it was leaning negatively though, last night reports came throughthat Iran have offered the US a fresh proposal to reopen the strait and end the war.However as Axios and others reported, this proposal postpones talks on nuclear capabilities.So it’s unclear whether the US Administration would tolerate that but for now the market is trading better than it might have done to start the week.This fresh development follows President Trump cancelling a planned visit to Islamabad by envoys Kushner and Witkoff, saying that the Iranians had “offered a lot, but not enough.”Iranian President Pezeshkian, meanwhile, said Iran would not agree to “imposed negotiations under threats or blockade.” The coming week will no doubt bring further developments, though predicting them is close to impossible. When the conflict began more than eight weeks ago, Reid - and many others - expected it to be comfortably over by now, with markets having followed the usual playbook and fully recovered.The market reaction has largely played out, but for the wrong reasons: the conflict is not over.That said, markets still appear to price in a meaningful chance that it will be resolved relatively soon. Polymarket, for example, suggests a 56% probability of traffic returning to normal by 30 June, although this briefly reached 91% ten days ago when it appeared that Iran was reopening the Strait.

In other news, one notable development yesterday wasSenator Thom Tillis’s decision to lift his block on Kevin Warsh’s nomination to chair the Fed.Tillis said he was satisfied with the Department of Justice’s decision late last week to drop its investigation into the Fed refurbishment. There had been some concern on Saturday that the DLooking ahead, with central bank meetings for every G7 country this week - alongside 42% of the S&P500 reporting by market capitalisation, including five of the Mag 7 - it is shaping up to be a blockbuster weekoJ had left the door open to reopening the probe at a later stage, which might not have been sufficient to clear the way. However, Tillis indicated that he had received assurances that gave him enough comfort to remove his block.

In terms of overnight markets, Brent crude is up +1.22%, marking the sixth consecutive session of gains, trading at $106.61 per barrel, following the weekend news. However regional equities are strong with theKOSPI (+2.57%) now at +57.6% YTD, largely on the back of two stocks: Samsung and SK Hynix.The Nikkei (+1.88%) is also strong. Other markets are a bit more subdued with the Hang Seng (+0.15%), the CSI (+0.21%), and the Shanghai Composite (+0.15%) slightly higher but with the S&P/ASX 200 (-0.14%) dipping.

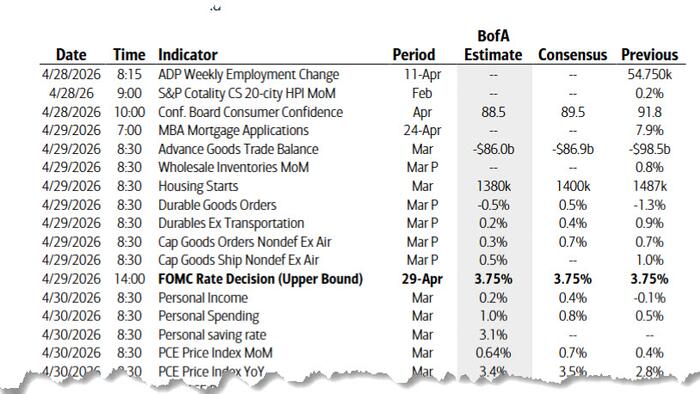

Looking ahead, with central bank meetings for every G7 country this week - alongside 42% of the S&P500 reporting by market capitalisation, including five of the Mag 7 - it is shaping up to be a blockbuster week, even before factoring in ongoing Iranian war newsflow.

The Bank of Japan meets tomorrow, followed by the Fed and the Bank of Canada on Wednesday. Thursday then brings decisions from the ECB and the Bank of England. All are expected to remain on hold, but the key question will be how each central bank’s reaction function is shaped by the conflict and the associated stagflation risks.

From an earnings perspective,22% of S&P500 market capitalization — across just four companies — reports after the close on Wednesday, when Alphabet, Microsoft, Amazon and Meta release their Q1 results. Apple follows on Thursday.

Turning to the Fed meeting mid week,Deutsche Bank economists’ base case is that any meaningful change in guidance is deferred until June, since this is Powell's last meeting. That said,there is a tangible risk that communication skews modestly hawkish — either through subtle language tweaks around “additional policy adjustments” or via Chair Powell signalling a more symmetrical assessment of risks to the dual mandate. An explicit acknowledgement that risks to price stability and employment are now more evenly balanced would likely be interpreted as a marginally less accommodative stance.

Geopolitics will loom large in Powell’s press conference, given developments in the Middle East.With uncertainty still elevated, Powell is likely to emphasise that policymakers cannot yet assess the precise implications for growth or inflation. However, he may also note that persistently high oil prices raise the risk of inflation becoming more entrenched over time.Overall, the tone should be consistent with a Fed prepared to remain on the sidelines for a while longer.

Alongside the meeting, Thursday’s personal income and spending report — and particularly core PCE — will be equally important. Income is expected to rebound by 0.6% after a 0.1% decline, while consumption is forecast to rise 0.5%.DB expects the core PCE deflator to increase by 0.25% month on month, lifting the year on year rate to around 3.13%. If realised, Q1 core PCE inflation will average just above 3.0%, marking five years since the Fed’s preferred underlying inflation gauge last ran at or below its 2% target.Our latest projections see core CPI and core PCE at 2.7% and 2.9% respectively by Q42026, highlighting how recent energy related shocks continue to complicate the path back to target.

Other data ahead of the meeting are unlikely to materially alter the Fed’s decision.Consumer confidence tomorrow is expected to fall to 88.8 from 91.9, reflecting heightened geopolitical concerns. More important than the headline will be the “jobs plentiful” and “jobs hard to get” components, which historically track movements in the unemployment rate and offer insight into perceived labour market momentum.

Source: ZeroHedge News