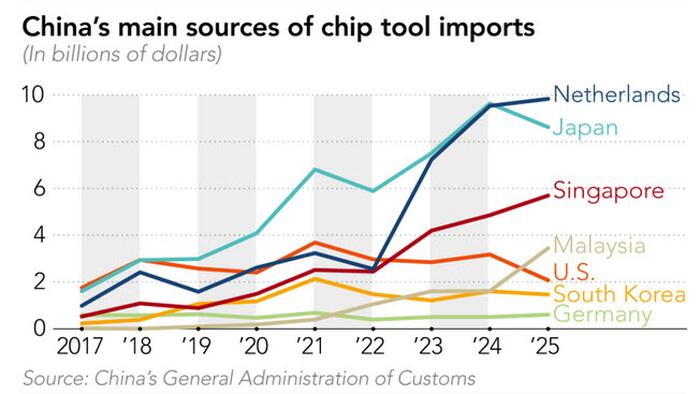

China's imports of chipmaking equipment from Malaysia and Singapore rose sharply in 2025 to surpass those from the US, which sank to an eight-year low, an analysis by Nikkei Asia has found - even as American companies remain a vital source of advanced tools for the country.

While the Netherlands and Japan remain China's primary foreign sources of critical semiconductor manufacturing machines by shipment origin, imports from the two Southeast Asian countries reached record levels:$5.7 billion for Singapore, up more than 17% year over year, and $3.4 billion for Malaysia, more than double the 2024 figure.

Direct imports from the US, meanwhile, declined more than 34% to about $2 billion, the lowest level since 2017, according to Chinese customs data. The decline was to be expected following President Trump's return to the White House, as he sharply limited access of US semiconductors to China, although tensions began earlier. Since Trump's first term and during the subsequent Biden administration, the US has raised tariffs and imposed fresh export controls aimed at slowing China's advances in chipmaking technologies for defense, space and artificial intelligence applications.

Despite the decline, the Chinese market remained a critical revenue source for leading US chip equipment makers last year.Applied Materials, Lam Research and KLA all earned more than 30% of their total sales from China in fiscal 2025.

Charles Shi, a veteran semiconductor analyst with Needham & Co., told Nikkei Asia thatthe uptick in China's imports from Southeast Asia is mainly due to the large number of U.S. chip equipment makers expanding manufacturing capacity in the region to better serve non-U.S. clients.

"Lam Research is building significant manufacturing capacity in Malaysia as they work to meet growing equipment demand beyond what their U.S. manufacturing capacity can serve," Shi said. "Singapore has been a popular destination for [the] U.S. equipment industry to go overseas. For example, both Applied Materials and KLA have been manufacturing in Singapore."

The three top U.S. chip tool makers generated nearly $19 billion in combined revenue from China in fiscal 2025, significantly exceeding figures implied by customs data based on where shipments originated from and underscoring the effectiveness of American vendors' production diversification strategies. Nikkei Asia first reported their productionshift toward Southeast Asiain early 2023.

For ASML of the Netherlands, China's share of revenue came to 29.1% in 2025, while the figure for top Japanese chip tool maker Tokyo Electron was more than 40% for fiscal 2025.

Anticipating major chip wars, over the course of 2020 to 2025,China's accumulated chip tool imports from Japan reached more than $42 billion, followed by the Netherlands' $35 billion. Japan is home to many top chip equipment makers such as Tokyo Electron, Screen Semiconductor Solutions and Ebara, while the Netherlands has the world's largest chip equipment maker, ASML, as well as key suppliers such as ASM, an atomic-level deposition tool specialist, and Besi, a maker of advanced chip packaging tools.

Meanwhile,China's domestic chipmaking equipment makers are experiencing a once-in-a-generation surge in growth, driven by Beijing's push to foster homegrown tools and reduce reliance on foreign technologies.Top suppliers all reported record revenue and profits for 2025, led by Naura, Advanced Micro-Fabrication Equipment Inc. China (AMEC), ACM Research and Piotech.

Source: ZeroHedge News