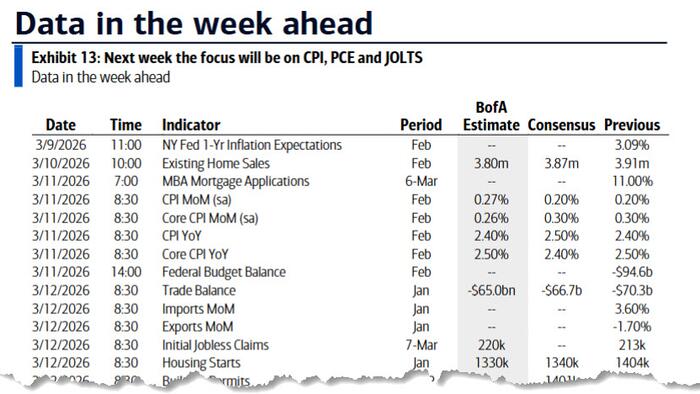

With the Fed in their self-imposed blackout period, the economic data will get a chance to do the talking ahead of the March 18th FOMC meeting. Of particular note will be the inflation data, namely Wednesday’s CPI report for February and Friday’s core PCE reading for January, but there will also be some scattered labor market data to help put context around last Friday’s disappointing February employment report. Of course, all of that assumes that traders can be dragged away from the latest Iran war headlines fro more than 5 minutes.

Turning to this week's main event,the February CPI report will get top billing. DB's expectations are for a 1.0% increase in energy prices to boost headline CPI (+0.27% forecast vs. +0.17% previous) relative to core (+0.24% vs. +0.30%). This translates to a year-over-year rate of 2.40% (vs. 2.39% previous), while the latter would tick down by 4bps to 2.46%. Within the CPI basket, DB looks for tariff-related strength in core goods, particularly apparel. In addition, recent gains in wholesale used car prices have the potential to begin adding to price pressures over the next couple of months. On the services side, expect more rental disinflation, though recent upward revisions to the repeat-rent indices suggest caution around the speed at which that can occur. Also look for payback from January’s particularly large increase in airfare prices, though recent moves in energy prices could add to airfares going forward.

Also of note on the inflation front this week will beFriday’s personal income (+0.4% forecast vs. +0.3% previous) and consumption (+0.1% vs. +0.4%) report for January,which will contain that month’s reading on core PCE, the Fed’s preferred inflation measure. Based on the January CPI and PPI data, DB is expecting a 0.42% increase (vs. +0.36%), which would take the year-over-year rate up a tenth to 3.1%. The Fed will have to wait until the morning of their March 18th meeting for the PPI data to get a more complete read on February’s core PCE. Based on our component-level CPI forecasts, our prior expectation is for a 0.18% February gain, which would have the year-over-year rate decline to 2.8%.

In terms of the labor market data,ADP’s weekly data on Tuesdaycovering the week of February 21st will provide an initial view on net hiring trends beyond February’s survey week. Similarly, Thursday’s jobless claims and Friday’s January JOLTs release will give additional context on gross labor market flows.

The remainder of the data this week will help forecasters sharpen their views on current quarter growth. Growth data will also feature. Revisions to the second estimate offourth quarter GDP(Friday) will update the baseline from which to judge early 2026 momentum. Tuesday’sexisting home sales(3.81mn vs. 3.91mn) for February and Thursday’s housing starts (1.325mn vs. 1.404mn) and permits (1.450 vs. 1.455mn) for January will provide an update on the residential sector. We will also get a preliminary look into the health of the factory sector withJanuary’s durable goods orders(+0.4% vs. -1.4% headline / +0.4% vs. +0.8% core) on Friday as well.

Friday will also see the preliminary release of theUniversity of Michigansurvey for March. While DB expects a decline in sentiment (55.0 vs. 56.6), due to the recent hostilities in the Middle East, also important for the Fed will be consumers’ inflation expectations.

Over in Europe, the focus will be on the monthly GDP for January in the UK (Friday), German January factory orders and industrial production (today) and the trade balance (tomorrow), and February CPIs in Norway and Denmark (both tomorrow).

Rounding out with earnings, there will be reports from Oracle and Adobe in the US as well as Inditex, Rheinmetall, Volkswagen and BMW in Europe. Finally, the focus will be on the Saudi Aramco earnings tomorrow amidst the big rise in oil prices last week.

The emergence of shale production in the US has helped to limit the impact of oil price spikes on the economy. Indeed, withinthe Fed’s FRB/US model, a $20/bbl increase in oil prices only increases unemployment by about 2bps and has almost no impact on core PCE inflation.However, with downside risks to the labor market while inflation has run above target for almost five years in a row, the response for the Fed to such a supply shock is not clear. Indeed, looking at the Fed’s prior responses to energy shocks does not yield a regular pattern (see “What does history tell us about the Fed's response to oil price shocks?”). Sometimes, the Fed emphasized the threat to the inflation side of their dual mandate while other times, it sought to protect against any deterioration in the labor market.

In the current episode, with inflation expected to be on a downward trajectory, the market could give the Fed some leeway to “look through” another supply-side shock. That said, inflation has been too high for too long, and the latest data calls into question how much disinflation can reasonably be expected, especially if there are increases in measures of inflation expectations (e.g., Friday’s Michigan data). On the flipside, growth looks strong but there are concerns on a forward-looking basis, for example, due to the potential for AI to disrupt the labor market.

Source: ZeroHedge News