The February jobs report is expected to show 55k jobs added to the US economy in the month, a sharp drop from 130k in January but slightly above the Fed's 50k breakeven estimate. Private payrolls are expected to rise by 60k versus the prior 172k. The unemployment rate is expected to remain unchanged at 4.3%, while wages are seen rising 0.3% M/M and 3.7% Y/Y. According toi Newsquawk, the data will be used to gauge Fed rate cut expectations, while some on the FOMC, including Waller, will use it to decide whether to vote for a rate cut or hold in March, although the Fed is expected to keep rates on hold barring any drastic change in the current situation or outlook.

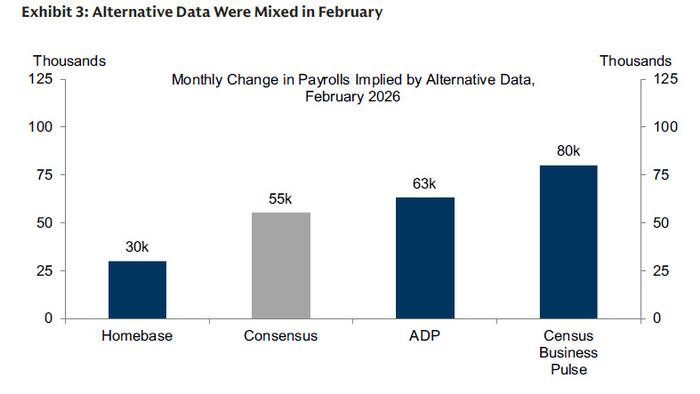

Recent proxies have been mixed: the ADP report was strong, while the ISM PMI employment sub-components showed improvement in both manufacturing and services, though manufacturing remained in contractionary territory. Initial jobless claims for the reference week were steady over comparable periods, while continuing claims rose slightly. The Conference Board reported a modest improvement in labor market perceptions. The Chicago Fed unemployment model expects the unemployment rate to remain at 4.3%.Earlier today, RevelioLabs reported 16.7k jobslostin February versus a 13.3k gain in January. Challenger layoffs fell notably.

Iran:Given recent developments in the Middle East, it is still too early to assess the impact on the US economy, thoughit could have implications for prices and, by extension, monetary policy.The Fed generally prefers to look through one-off energy-related price increases. However, if the war is prolonged and disruption persists in the Strait of Hormuz, there is a risk this could delay the resumption of rate cuts, which are currently expected in the summer. A sharp deterioration in the labor market would likely offset these concerns, but the situation keeps the Fed in a difficult position. The US has offered to assist shippers and tankers transiting the Strait by paying for insurance and providing US Navy escorts. This is a new announcement and its effectiveness remains to be seen, but if successful it could help shield the global economy by keeping supply chains and oil flows open. Market-based inflation expectations remain anchored. As of 4th March, the 5-year breakeven rate stood at 2.46%, up from 2.40% on 27th February, while the 10-year rate is at 2.29% versus 2.25% at the end of last-week

Arguing for a weaker-than-expected report:

Arguing for a stronger-than-expected report:

Updated Population Controls:Tomorrow's update will re-anchor the survey’s population estimate to the newly released Census population estimate, resulting in one-time adjustments to the levels of the labor force, employment, and other series in February. The household survey has likelyoverstated population and employment growth over the last yearbecause the survey’s population assumptions quickly became outdated as immigration continued to fall sharply. We estimate that this will result in downward adjustments to the labor force and employment of 0.3-0.4mn (Chart below, left panel). The annual update will also likely have a tiny composition effect on ratios like the unemployment rate. That becauserecent immigrants are more likely to be young Hispanics and young Asians,who tend to have higher labor force participation and unemployment rates than the population average. As a result, a disproportionate decline in the population size of these groups will lower these rates. However, because the magnitude of the revision is relatively small, the participation rate and employment-population ratio will decline by only 1-2bp and the unemployment rate to be essentially unchanged (Chart below, right panel).

Fed:The Fed is currently on hold and views among FOMC participants remain mixed, with some officials objecting to further rate cuts while others would prefer the easing to continue. Overall, the outlook largely depends on incoming data and how far the Fed is from both sides of its mandate. The labor market has stabilized in recent months, while inflation remains above target, largely supporting the case for rates to remain at current levels. This report will be key in assessing whether Januaryʼs labor market strength is sustained and whether the view that the labor market has stabilized still holds. Large downward revisions or a notably weak report would boost dovish rate expectations and strengthen the case among doves for cuts to resume sooner rather than later. Fed Governor Waller, a dovish dissenter, said he would support a cut in March if Januaryʼs labour market strength is revised away or fades, though it may be appropriate to hold if downside labour market risks have diminished. Governor Miran, an uber dove, wants four 25bps cuts this year, sooner rather than later. New York Fed President Williams has said rate cuts will continue if inflation ebbs. Goolsbee (non-voter this year) is optimistic about more cuts this year but wants clear evidence inflation is returning to target first, specifically warning about persistently high core services inflation.The Fedʼs median dot plot pencils in one rate cut in 2026, taking the target range for the federal funds rate to 3.25-3.50% by year-end, though the Summary of Economic Projections will be updated at the next Fed decision on March 18th.

For options expiring on March 6, the market is pricing +/-1.14% move, as of market close on March.

JPM Market Intel:According to the JPM trading desk,the range of SPX outcomes is skewed lower given the uncertainty around the US / Iran war.The heightened oil market and general market vol is not bleeding into the NFP print, which may be muted given the expectations for a weaker Retail Sales number. For this print,the stronger the better given the increase in inflation expectations due to energy prices. A weaker number will increase rate cut expectations, but the risk is stagflation in the near-term given the expected increase in inflation.If the US / Iran war were to resolve overnight, the US economy is on solid footing with positive growth momentum, evidenced by the ISM prints. JPM remains of the view thatreduced uncertainty on taxes and tariff rates that continue to trend lower benefits the economy and is likely to translate into improved hiring.If that comes to fruition then consumer will continue to drive the economy to above-trend growth, benefiting earnings and risk assets.The trade off is zero rate cuts this year.

Below JPM's trademark market reaction matrix:

Source: ZeroHedge News