It will come as a surprise to exactly nobody that the Fed's latest quarterly Household Debt and Credit report (for Q4 2025) reported total household debt balances increased by $191 billion in the fourth quarter of 2025, a 1% rise from 2025 Q3, to a new all-time high.Balances now stand at $18.8 trillion and have increased by $4.6 trillion since the end of 2019, just before the pandemic recession.

This is how various debt balances changed through the quarter:

New debt originations were also solid in the quarter:

Taking a closer look at some of the negative changes below the surface,delinquency rates on loans ranging from mortgages to credit cards rose to 4.8% of all outstanding US household debt in the fourth quarter, up 0.3% sine Q3 2025 and the highest level since 2017, driven by higher defaults among low-income and young borrowers.

As Bloomberg notes, while the overall share of loans in some stage of default is near pre-pandemic averages, the rise in delinquencies among the lowest earners adds to evidence of an increasingly K-shaped economy, and nowhere was it more obvious than in the case of student loans - where with the Biden repayment moratorium has been over for the past year - we have seen a tsunami of both early delinquencies,with 16.3% of student-loan debt became delinquent in Q4 the biggest increase on record in data going back to 2004...

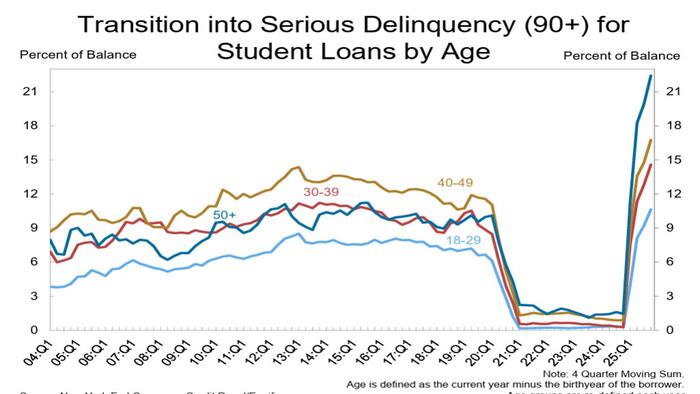

... and serious delinquencies (effectively defaults)...

... led by50+ year-old "students"(almost certainly of the liberal major, blue-haired anti-ICE, variety).

The rise in defaults was also driven by delinquencies in mortgage payments, and New York Fed researchers found that they were particularly high in lower income zip codes.

“As household debt levels grow modestly, mortgage delinquencies continue to increase,” said Wilbert van der Klaauw, an economic research advisor at the New York Fed, said in a press release accompanying the figures. “Delinquency rates for mortgages are near historically normal levels, but the deterioration is concentrated in lower-income areas and in areas with declining home prices.”

The increased struggle in low-income and young borrowers’ ability to pay their loans is consistent with elevated unemployment rates among some parts of the population, the NY Fed researchers added. The jobless rate for workers 16 to 24 years old stood at 10.4% in December, near the highest levels since the depths of the pandemic in 2021, and largely the result of AI disruption.

Source: ZeroHedge News