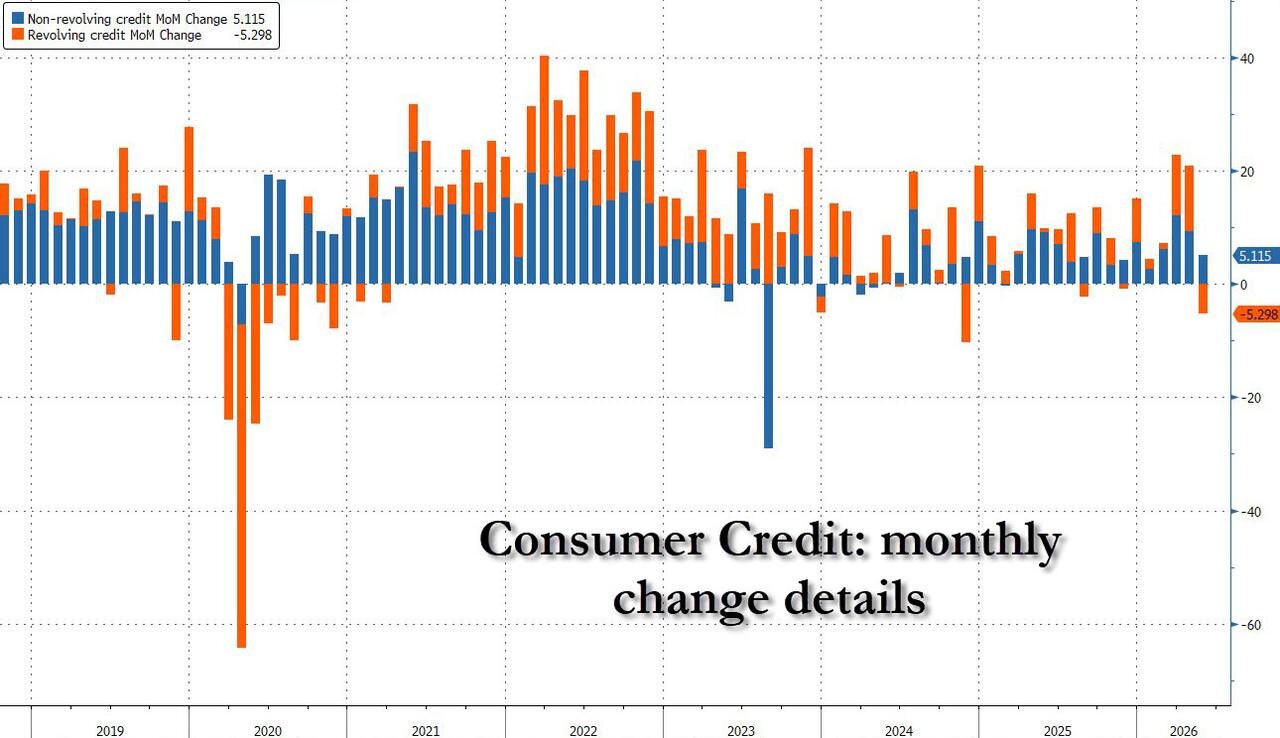

After two consecutive outsized jumps in consumer credit in the months of March and April, when gas prices surged and inflation resumed its track higher, lifting most prices as a result of the war in Iran, moments ago the Fed published its latest consumer credit (G.19) report for the month of May and it was a doozy: instead of the expected $17.5BN increase, in May total consumer credit unexpectedly shrank for the first time since November 2024.

{kind=link}

The move was driven by a notable slowdown in nonrevolving credit, coupled with the biggest drop in revolving (credit card) debt since late 2024.

{kind=link}

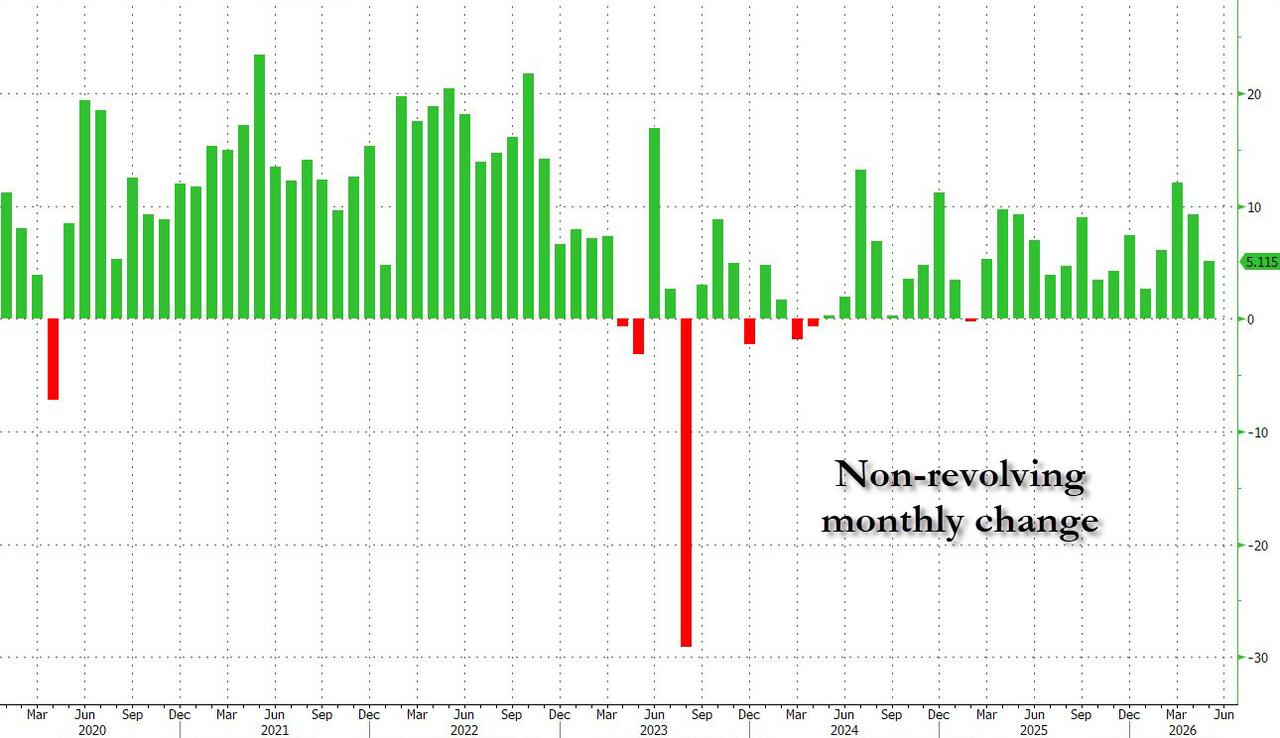

Specifically, car and student loans (collectively non-revolving credit), rose by a modest $5.1 billion.

{kind=link}

It was unclear what was behind the muted rise: recall that for the first quarter of 2026, student loans surged by $28 billion while auto loans posted a $2.4 billion decline, perhaps due to the very high interest rates on the debt (we will get an update for Q2 next month).

What is interesting, is that while auto loans have barely budged since late 2023, staying around 1.55 trillion for nearly three years, student loans have resumed their ascent, and after a modest decline in late 2023, student loans are once again at all time highs just shy of $1.9 trillion. <