By Benjamin Picton, senior market strategist at Rabobank

When A Toll Isn't A Toll

Yields on 10-year Treasuries finished last week up 11bps to 4.48% while yields on 10-year Bunds rose 8.5bps to 2.93%. Those higher borrowing costs came despite signs of weakening in the US jobs market, a weaker-than-expected prices paid figure on the ISM manufacturing index, and a surprisingly weak Eurozone CPI inflation report that follows in the wake of lower than expected inflation readings in the UK.

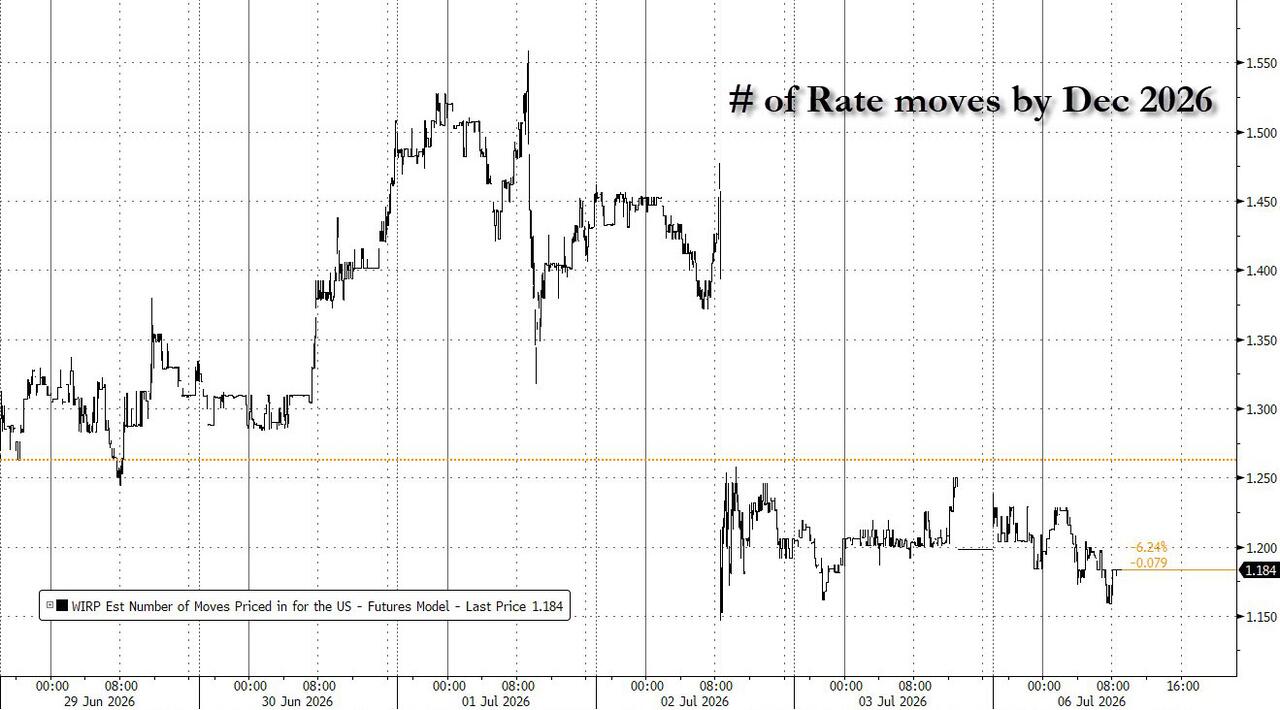

Market-based expectations of the future path of the Fed Funds rate finished the week a little lower than it started, with pricing of a future rate hike pushed out from October to December. 2-year Treasury yields fell by almost 4bps on Thursday after the payrolls report confirmed hiring in June was little better than half the expected figure.

{kind=link}

This was still enough for the unemployment rate to tick down to 4.2% as a lower participation rate saw the labor force contract. Nevertheless, 2-year yields were higher across the week as sovereign curves bear-steepened.

Brent crude posted its first weekly gain in almost a month last week to see the front contract close up 0.18% at $72.12/bbl. The gains appear to have been short-lived as news of continued tanker flows through the Strait of Hormuz and a decision by OPEC+ over the weekend to ease production restrictions by 188,000 barrels/day from August steer the price action lower this morning. Announcements of increased production are all well and good, but when much of that production is occurring in the Persian Gulf or in Russia (where Ukrainian strikes against oil infrastructure are ongoing) the ability to actually ship the product to market will remain the cri