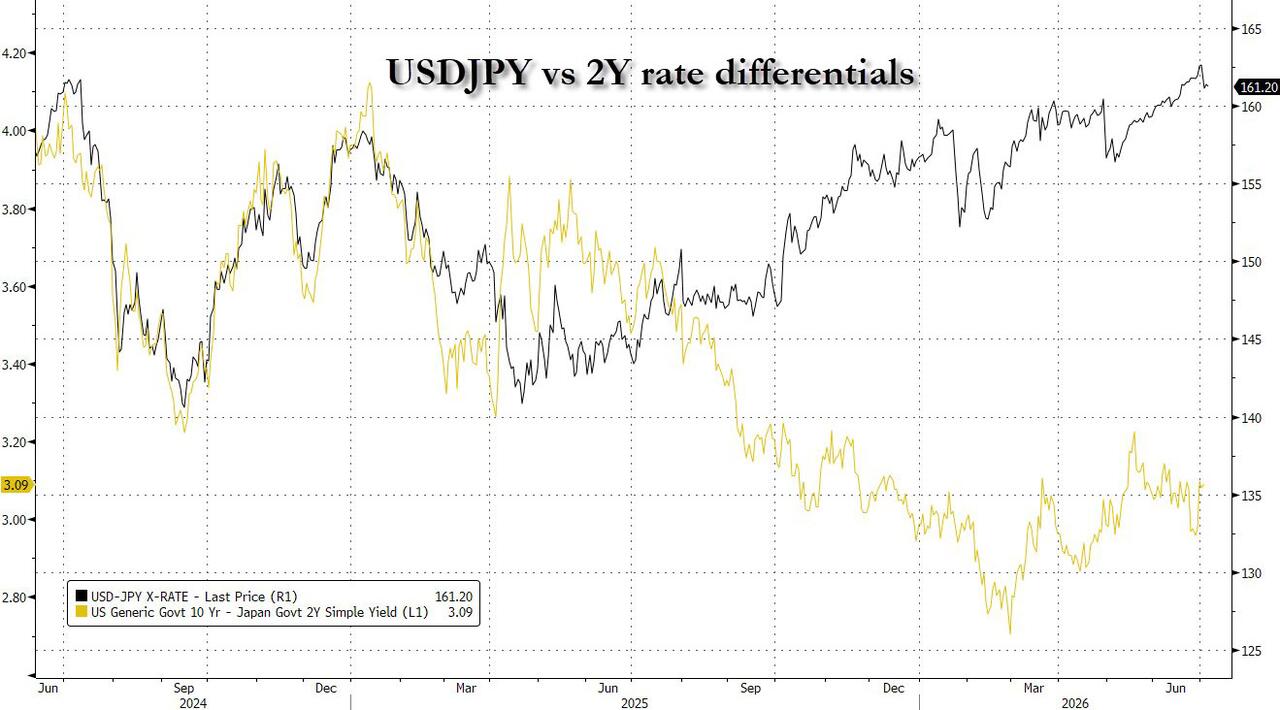

In recent months one of the more frequent questions in FX trading has been the relentless collapse in the yen, which recently sank below a 40 year low despite rate differentials stubbornly headed in the opposite direction, and is increasingly flirting with levels which on previous occasions always prompted BOJ intervention.

{kind=link}

Among the reasons cited for the chronic weakness of the Japanese currency have been the following three:

- Real short-term rates in Japan are negative, which is why Ueda has been slow to hike

- There is a growing perception that Japan's PM Takaichi doesn't want a higher rates or a stronger yen. A weak yen certainly helps big JP firms profits (while hurting households) so there is a clear weak yen constituency inside the LDP. Japanese financial institutions are also short the yen generally

- JP financial institutions (notably lifer insurers) see the upfront cost of hedging (the nominal ST rate differential) and have made a mint on unhedged fx assets, and they have been reluctant to change their position just because the yen looks exceptionally undervalued.

Effectively a feedback loop has emerged, whereby the weaker yen leads to an even weaker yen, and despite token resistance by the BOJ - the latest long overdue rate hike being an example - the market clearly anticipates further weakness in the currency, and is pushing it to new lows.

However, a limit to the yen's weakness is now emerging, and it goes to the growing damage on the country's households noted in point 2 above.

As Bloomberg reports, Japan’s weak currency caused the most bankrup