German Chancellor Friedrich Merz appears disoriented, whiny-apathetic, and remarkably weak in leadership these days. Perhaps the chancellor senses that the project of his political generation is entering its final phase. Is he aware that the construction of eco-socialism has failed? That both his reckless debt policies and Germany’s rapid deindustrialization are consequences of this ideological insanity? The fact that Friedrich Merz still found the audacity — despite the catastrophic domestic political and economic situation at home — to publicly accuse U.S. President Donald Trump of lacking strategy in the Iran conflict speaks to an almost immeasurable degree of stubborn arrogance and self-delusion.

There he was again: the German know-it-all.The type of politician who once lectured Europe’s neighbors over debt problems while failing to compare his own actions with the present condition of his own country.

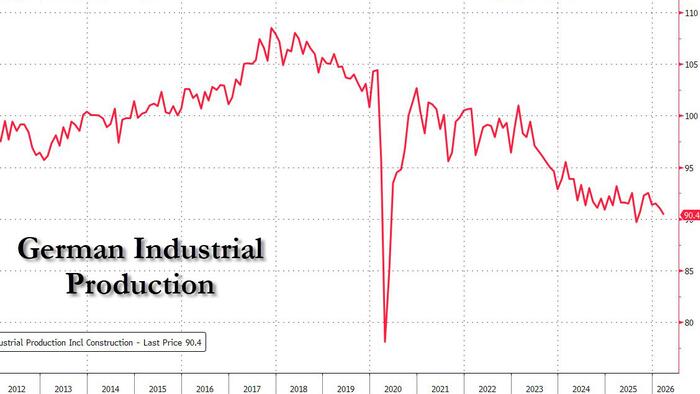

Merz would have done well to take a look at the American economy and the U.S. labor market before stepping onto such embarrassingly thin rhetorical ice.

In April, the private sector in the United Statescreated 115,000 new jobs. During the opening months of the previous year, another roughly 180,000 jobs had already been added. The U.S. economy has now delivered four strong months in a row, signaling that America is rapidly gaining momentum and — unlike the European economy — is not being derailed by the Iran crisis. These are phenomenal numbers at a time when the world is fighting over scarce capital, know-how, and access to cheap energy resources.

The contrast with Germany could hardly be greater. During the first year of the Merz government, the German public sector was bloated with another 205,000 more-or-less useless jobs, while Donald Trump’s administration cut 300,000 positions from the overstretched state apparatus. During the same period, the American private sector created a net total of more than 750,000 jobs since Trump returned to office, while the German economy eliminated roughly 200,000 positions.

Deregulation, tax cuts, and a fundamental trust in the power of private enterprise across the Atlantic stand in sharp contrast to the sluggish, apathetic-socialist policies of Germany and the European Union — and not in Europe’s favor.

How strongly the American economy is currently developing can be seen in an interesting media phenomenon.

April 29, 2026 - a Wednesday - may one day prove to have been an important turning point. On that day, outgoing Federal Reserve Chairman Jerome Powell appeared before the press for the final time to announce the latest decision on U.S. interest rates. The fact that the Fed left rates unchanged within a range of 3.5 to 3.75 percent came as no surprise. What was striking, however, was the deafening silence inside financial newsrooms, which normally inflate Fed rate decisions into mega-events for the markets and American capitalism itself. This time, the waters remained perfectly calm.

Two developments lie behind the media’s sudden disenchantment with Fed meetings. First, there is the policy of U.S. Treasury Secretary Scott Bessent, who used legislation such as the Genius Act and the Clarity Act to establish the framework for U.S. dollar-based stablecoins, thereby shifting a significant portion of money creation back into the hands of the private banking sector — where it once resided before the creation of the Federal Reserve. Second, the higher policy rates compared to the Eurozone appear to indicate that the U.S. economy is far more robust than European politicians and media figures would like to admit.So the attitude has become: best not to talk about it too much. Otherwise, people might start noticing that the Eurozone economy itself is incapable of surviving positive real interest rates.

Donald Trump’s second presidency has so far delivered 15 months of determined deregulation and a noticeable liberation of the energy sector from the strangling regulatory activism of climate fanatics. Until Trump’s election victory, Washington had been ideologically subordinate to Europe. Back in 2009, the Europeans succeeded in pushing Barack Obama into effectively adopting Europe’s climate policies wholesale in the United States. But the hope that America’s collapse would somehow conceal Europe’s own decline has now evaporated. Behind the strength of the U.S. labor market stand massive forces of private-sector investment.

Source: ZeroHedge News