SSDD: with stocks set to hit new record highs, the hope this morning once again is that the days may be numbered for the war in Iran, with momentum building since the start of the weekend that a deal could be in the works. Brent, which ended last week at $103.54/bbl, is this morning trading at $97.87/bbl, around -5.48% lower than Friday’s close. However, Brent had got as low as $96.02 late yesterday before news overnight that US and Israeli jets conducted fresh strikes in Southern Iran, hitting missile launch sites and mine-laying boats. These actions were described as "defensive" and not an end to the ceasefire with Iran.

Net net,optimism is still elevated that an agreement can be made to end the war.We have been here before, of course, but it has felt for some time that the move towards peace has been three steps forward and one or two back. It is now 48 days since the main kinetic encounters, and according to DB's Jim Reid, such a prolonged truce and ceasefire would not have held if the US genuinely wanted to continue strikes, unless there was absolutely no alternative. Last night's targeted action is clearly a warning shot that the ceasefire is fragile though, so we will have to see what the next few days of negotiations bring.

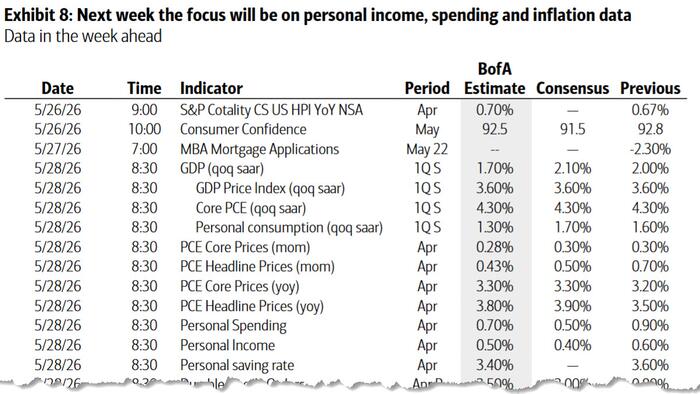

Moving on to the rest of this week, inflation once again dominates with important price data across the US, Europe and Japan.In the US, the clear focal point is Thursday’s April personal income and spending report (Thursday),which contains the Fed’s preferred inflation gauge. DB economists expectcore PCE inflation at around +0.3% month-on-month, unchanged from March, with the year-on-year rate edging higher.This release matters not just for the inflation print itself, but for how it fits with the broader narrative of sticky services inflation and resilient demand.

On the real economy side of the same report (Thursday), economists expect momentum to cool after a very strong March, withpersonal consumption growth slowing back to around +0.3% month-on-month and personal income rising by roughly +0.4%.This comes after ahawkish speech from Waller on Friday.He discussed how the recent labor market and inflation data had caused him to reevaluate the balance of risks with inflation becoming the “driving force” behind monetary policy in the near term. In particular, he noted thathe would support changing language in the statement to remove the easing bias and make it clear that “a rate cut is no more likely in the future than a rate increase”.In light of this there is a lot of Fedspeak to watch this week. You can see a list in the day-by-day calendar at the end as usual butkeep an eye on Minneapolis’s Kashkari (today) and Dallas’s Logan (tomorrow),both of whom had dissented against the easing bias in the April statement. They are likely to repeat their view that the stance of monetary policy should be more balanced, particularly as inflation risks remain front of mind.

Staying with the Fed, last Friday, DB's Chief US economist, Matt Luzzetti, wrote an interesting piece entitled “overinsured” where he discusses how the Fed has delivered175bps of rate cuts in this cycle even as inflation has remained well above target,framing the last round as “insurance” or “risk management” cuts in response to elevated downside labor market risks. Matt suggests that relative to a set of standard policy rules, the first set of cuts in 2024 was appropriate. But following the second set last year, and the recent acceleration of inflation,the fed funds rate is now significantly below all policy rule settings. This finding is robust to different plausible estimates of r-star and the use of economic forecasts instead of current inflation and unemployment in the policy rules.

Beyond PCE,Thursday also brings durable goods orders (Thursday),where our economists look for a modest headline increase consistent with steady but unspectacular capital spending momentum. Earlier in the week,the Conference Board’s consumer confidence index (tomorrow) is expected to edge lower, potentially reflecting the cumulative impact of higher rates and policy uncertainty.Weekly initial jobless claims (Thursday) remain an important high-frequency signalon labor market conditions, although holiday effects may add some volatility.

In Europe, attention turns tothe May flash inflation prints at the end of the week,with Germany, France, Italy and Spain all reporting on Friday, ahead of the Eurozone aggregate the following week. DB economists expect inflation to remain above target across the region. Alongside the data, theECB publishes the account of its April meeting (Thursday) and its Financial Stability Review (Wednesday),offering further insight into how policymakers are balancing lingering inflation pressures against softer growth and financial stability considerations.

In Asia, Japan is the key focus.Friday’s Tokyo CPI (Friday) will provide an early read on national inflation trends,alongside April industrial production and retail sales (Friday). Our economists expect inflation measures to firm modestly, underscoring that price pressures remain present even as activity data stay mixed. Elsewhere,China releases industrial profits (tomorrow), Australia publishes its April CPI (Wednesday), and the RBNZ announces its latest policy decision (tomorrow),where most economists expect the cash rate to be left unchanged.

On the corporate side, earnings highlights include US tech names such as Dell, Marvell and Salesforce, alongside consumer-facing firms including Costco and Dollar Tree, with most results clustered around mid-to-late week.

Courtesy of DB, here is a day-by-day calendar of events

Source: ZeroHedge News