Two weeks ago, when discussing the market "mystery" of sliding physical crude oil prices, we said that the most likely culprit were Chinese refiners, whose refining margins had just collapsed to the most negative on record.

The reason for the margin collapse was China’s domestic fuel policy: it has long been Beijing's policy to soften price hikes to help shield consumers and avoid social unrest; which while beneficial to end, consumers is catastrophic to refiners and processors who are prohibited from passing on rising costs. In other words, Chna’s "energy security" was the dominant theme, and if it meant an entire industry has to suffer huge losses if it continues to purchase oil and process it into various product grades, so be it.

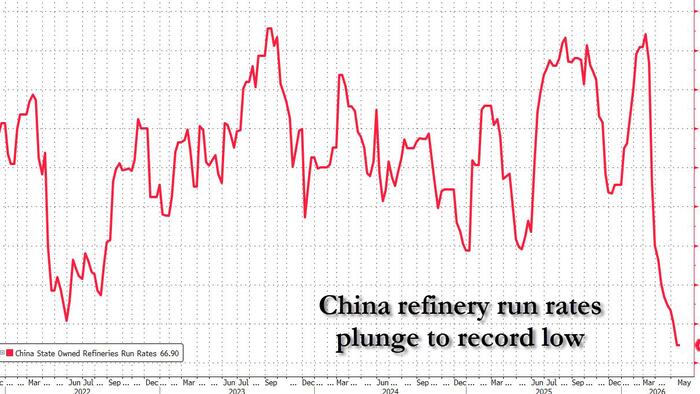

Ordered to process as much available inventory as possible, that's what the refiners have done, and refining rates in Shandong province, China's hub for smaller refineries known as teapots, ramped up over April to the highest level in almost two years, as processing margins cratered to record negative levels meaningrefiners are losing record amounts on every barrel they process.

“I would not be surprised if the teapots are prioritizing politics over economics with an eye to their long-term survival,”said Erica Downs, a senior research scholar at Columbia University’s Center on Global Energy Policy. “They may be calculating that if they do their part to help China weather the energy crisis, then maybe they will build up some goodwill in Beijing.”

While Downs is right, and teapots are prioritizing politics, they are also certainly keeping an eye on economics to the extent they can avoid Beijing's wrath, and predictably the logical consequence of this centrally-planned policy to force "independent" refiners (who are not really independent if they have to do whatever Beijing instructs them) to make fuel at record losses to ensure energy security,is for them to slash purchases of Iranian crude.

Sure enough, as we reported two weeks ago, Chinese crude oil imports cratered: China's April imports plunged to a multi-year low of just 8.2 million barrels a day, down by about a quarter from a prewar level of around 11.7 million. The 3.5-million barrels a day swing almost matches the total consumption of Japan and isdouble the amount supplied by the United Arab Emirates pipeline that circumvents Hormuz.

Meanwhile, as imports collapsed, inventories at sea soared: Kpler reported that as of the start of May, there were about16 million barrels on ships anchored in the Yellow Sea off the Chinese coast, almost 40% higher than the level prior to a US blockade of Iran’s ports in mid-April as oil that was ordered previously remains unused.

Amid this collapse in Chinese imports and aggressive stockpiling at sea, industry executives have noticed something odd:Chinese state-owned oil companies have been reselling some of their oil cargoes to European and Asian rivals.The behavior suggests surpluses, which is "odd" to say the least during a supply shortage. Where is this excess oil coming from?

The shift has not only capped benchmark oil prices,but also helped to trigger a collapse in the premia that traders pay above them to secure physical crude.The immediate outcome has been a very beneficial one:physical barrels that in early April went for $30 above benchmark prices were recently changing hands at premiums as low as $1. Talk of discounts has even started to emerge.

Underscoring this point, North Sea oil traders were no longer desperate for crude for immediate delivery anymore, compared to the panic buying of late March and early April

Source: ZeroHedge News