By Teeuwe Mevissen, Senior Macro Strategist at Rabobank

Since the start of the Iran war the market has had a tendency to view the likelihood of a peace agreement with a ‘glass half full’ attitude.

Once again, markets have found some comfort in encouraging remarks from both the US and Iran, even though both sides are making it clear that there are still major sticking points on critical issues.

US Secretary of State Rubio has suggested that there are “some goods signs” towards finding a resolution. This is despite Iran’s Supreme leader ordering that the country’s enriched uranium must not be sent abroad, which is a key objective of both the US and Israel. Rubio has also stated that any deal that involved Iran imposing tolls on shipping passing through the Strait of Hormuz would be unacceptable. This statement comes on the heels of this week’s news that Iran is looking to set up a new“Persian Gulf Strait Authority”to exert control over a maritime zone in the area and that the country’s authorities are also discussing with Oman how to set up a permanent toll system. Amid the confusion over the degree of progress towards peace, Brent crude prices have ticked higher this morning, though they remain in the lower part of this week’s range.

Reflecting movements in oil prices, US treasury yields are also trading in the lower part of this week’s range, though they remain at elevated levels. While asset prices continue to take their cue from speculation regarding the length of time that the Strait of Hormuz may be closed,economic data are increasingly reflecting the impact that the supply shock is already having.

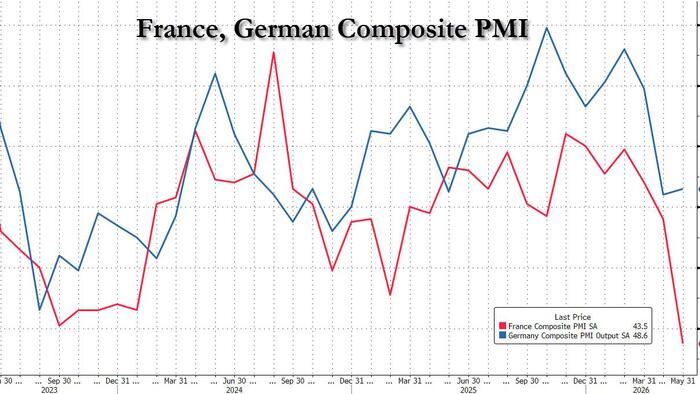

Yesterday’s release of French preliminary MayPMI data showed a plunge in the composite number to 43.5 from 47.6 the previous month,with weakness evident in both the manufacturing and the services sectors.The composite number, which is a 66-month low, would usually be associated with recession.

According to S&P Global,firms cited higher fuel and energy costs as reasons for lower output, with manufacturing firms citing material shortages.

The German PMI data was less of a shock but with a composite number reading 48.6, the economy is continuing to show signs of contraction. While this morning’s German IFO release was a little better than expected, it remains close to a 5-year low.

Yesterday’s release of the spring forecasts from the European Commission reflected the growing pessimism regarding the economic toll of the Iran war. GDP growth in the EU is now projected to slow to 1.1% in 2026, a downward revision of 0.3 ppts from the autumn forecasting round.

Growth for the Eurozone this year is now projected to be just 0.9%, while price pressures have been revised higher. The EC’s forecast for inflation in the EU has been revised a full percentage point higher to 3.1% in 2026. The forecast for the Eurozone stands at 3% this year up from an autumn forecast of 1.9%.

Source: ZeroHedge News