Looking at the week ahead,Nvidia’s earningson Wednesday, with a market capitalisation now of $5.46tn, will be the main event. In economics, we have the global flash PMIs on Thursday, along with inflation data from Canada tomorrow, the UK on Wednesday, and Japan on Friday. From central banks, the highlight will be the FOMC minutes on Wednesday. Those flash PMIs will be important, as they’re one of the first indicators on how the global economy has performed this month, so will be scrutinized for any signs of how the war in Iran is impacting activity and prices.

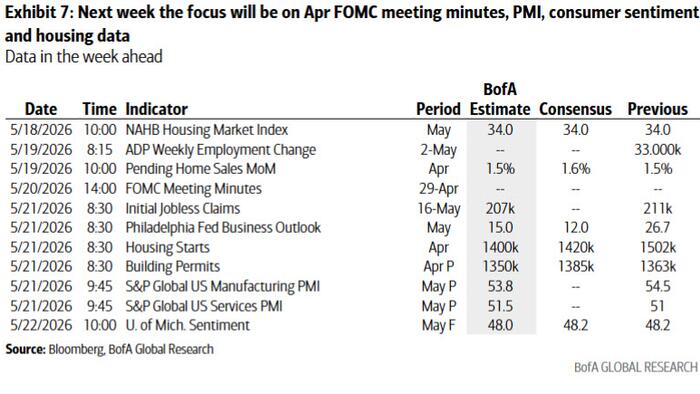

The US calendar is relatively light,with the NAHB housing market indextoday expected to remain unchanged at a cyclically low 34, followed byTuesday’s pending home sales, where a modest +1.0% increase is anticipated (from +1.5% previously). Attention will then turn toThursday’s April housing activity data, where housing starts are expected to ease to an annualized pace of 1.425mn (from 1.502mn), while permits are projected to tick higher to 1.375mn (from 1.363mn). All estimates are according to our economists.

Beyond housing,Thursday is the key day for macro releases. The weekly initial jobless claims are expected to edge slightly lower to 209k (from 211k). The same day will also bring the Philadelphia Fed manufacturing survey, where our economists expect a pullback to +21.0 (from +26.7),alongside the flash PMIs. In the US, manufacturing is expected to soften marginally to 53.7 (from 54.5), while services are seen ticking up to 51.5 (from 51.0).

In contrast to consumer sentiment—which will see an updated reading of the Michigan survey on Friday (expected at 48.2 versus 49.8 previously)—business surveys have generally remained more resilient despite the energy shock. That said, some indicators have shown rising input costs and lengthening delivery times, developments that could signal renewed inflationary pressure building beneath the surface.

Turning to central bank communications,the Fed speaker slate is relatively limited but still notable. Governor Waller is scheduled to participate in an ECB policy panel tomorrow, alongside comments from Philadelphia Fed President Harker (voter) on the outlook. On Wednesday, Vice Chair Barr will discuss consumer financial health metrics, while the Fed will also publish the minutes from the April FOMC meeting. Richmond Fed President Barkin (non-voter) will follow on Thursday with remarks on the economy, before Governor Waller rounds out the week with a further appearance on Friday.

In Europe,the highlights will include the UK labour market report tomorrow and inflation data on Wednesday. DB's UK economist expects headline CPI to slow to 2.98% YoY and core CPI to fall to 2.61% YoY. More detail and forecasts are in the full inflation spotlight note here. The UK will also release the GfK May consumer confidence index and April retail sales on Friday.Other notable European releases include Eurozone consumer confidence on Thursday and Germany’s Ifo survey on Friday.

In Asia, Japan faces a busy week, with key data including Q1 GDP tomorrow and April nationwide CPI on Friday. Our Chief Japan economist expects positive real growth of an annualised 1.3% QoQ for the GDP report and sees core CPI inflation, excluding fresh food, holding at 1.8% YoY, alongside a retreat in core-core inflation, excluding fresh food and energy, to 2.2% (from 2.4% in March).

Finally, beyond Nvidia’s earnings on Wednesday, results are also due from major US retailers, including Walmart, Home Depot, and TJX.

Courtesy of DB, here is a day by day calendar of the week's main events:

Taking a look at just the US, Goldman writes that the key economic data release this week is the Philadelphia Fed manufacturing index on Thursday. There are several speaking engagements with Fed officials this week, including events with Governors Waller and Barr and Presidents Paulson and Barkin. The minutes to the FOMC’s April meeting will be released on Wednesday.

Source: ZeroHedge News