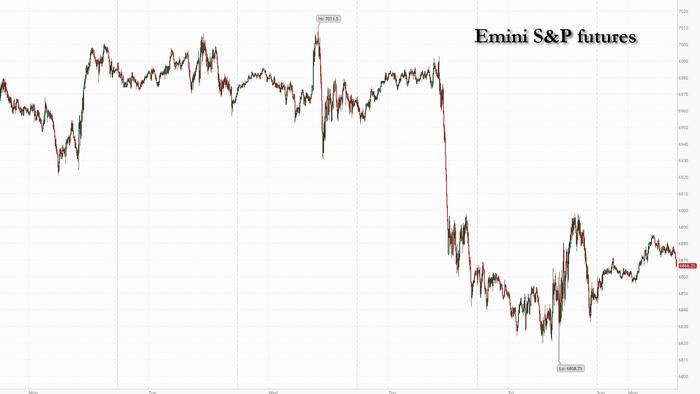

Stocks gained, bitcoin tumbled and bonds steadied after Friday's cool CPI data reinforced expectations that the Fed will cut interest rates on multiple occasions this year. With US markets closed for the Presidents’ Day holiday and mainland China’s markets closed for Lunar New Year holidays, trading was muted on Monday. As of 9:00am ET, futures on the S&P 500 added 0.4% and Europe’s Stoxx 600 index rose 0.4% as banking shares rebounded from a sharp decline last week. German bunds and Treasury futures were steady after US yields touched the lowest since December on Friday.

The path of US interest rates remains in focus following Friday’s slower-than-expected US inflation print as traders fully price a Fed cut in July and the strong chance of a move in June.

“The backdrop for equities is positive post CPI,” said Andrea Gabellone, head of global equities at KBC Securities. At the same time, there could be “more dispersion ahead as sentiment around key AI-exposed sectors is still very critical,” he added.

That sentiment was echoed by other strategists seeking to distinguish between AI losers and winners.

A JPMorgan Chase & Co. team led by Mislav Matejka urged caution on stocks at risk of AI-driven “cannibalization,” including software, business services and media companies. Meanwhile, banks are developing baskets to capitalize on the divergence: as wefirst reported last Thursday,Goldman launched a new basket of software stocks that goes long firms that will benefit from AI adoption, while shorting the companies whose workflows could be replaced.

With AI disruption rippling through markets, a lot will come down to earnings resilience, in particular in the US.

“When you look at the current earnings season, the companies are showing 13% of growth,” Nataliia Lipikhina, head of EMEA equity strategy at JPMorgan, told Bloomberg TV. “Overall, this is the reason why we continue to be positive on the S&P.”

Later this week, traders will be watching for ADP private payrolls numbers on Tuesday and the minutes from the Fed’s January meeting on Wednesday for a fresh read on the economy.

European stocks gained with bank shares rebounding, after posting their biggest weekly decline since April on worries about disruption from artificial intelligence. The basic resources sector lags, with Norsk Hydro among Europe’s worst performers as both Goldman Sachs and RBC downgrade the stock. Stoxx 600 rises 0.4% to 620.26 with 253 members down, 336 up, and 11 unchanged. Here are some of the biggest movers on Monday:

Asian stocks slipped for a second day, led by declines in Japan as traders booked profits after last week’s post-election rally. Several markets were closed or held shortened trading sessions for the Lunar New Year holiday. The MSCI Asia Pacific Index was down 0.1%. Japan’s Topix Index fell 0.8%, with Mizuho Financial Group Inc. and Toyota Motor Corp. among the companies contributing to the index’s losses.In Hong Kong, AI model developer Minimax Group Inc. surged as much as 30% to more than four times its original listing price, while competitor Knowledge Atlas JSC Ltd. ended 4.7% higher. The market will be closed until Thursday. As investors across the region begin to reevaluate their bets on its artificial-intelligence-driven rally, traders in Japan cashed in gains driven by expectations of Prime Minister Sanae Takaichi’s proactive spending policies last week.Trading in Singapore ended early Monday and will be shut until Wednesday. Equity markets in mainland China, South Korea, Indonesia and Vietnam were closed.

Source: ZeroHedge News