Submitted byQTR's Fringe Finance

What a week for macroeconomic data. We got two horrific datapoints this week that, when combined with some key comments from days ago, seem to be pushing the Fed closer to rate hikes than they’ve been in a long while.

The case for rate hikes is no longer some fringe tail risk like it felt it was a year ago as inflation numbers (though still high) appeared to be coming down.

For most of last year, markets were operating under a very clean narrative that inflation would continue cooling, growth would gradually slow, and the Federal Reserve would eventually be in position to cut rates further. That framework is starting to crack.

Regardless of whether investors were focused on a potentially more dovish policy direction under figures like Kevin Warsh or Stephen Miran, the Fed ultimately cannot sidestep hard inflation data. If price pressures are clearly reaccelerating, policymakers risk losing massive credibility if they continue signaling easing while inflation moves in the opposite direction.

The market is being forced to confront that reality in real time. And this chart from Charlie Bilello yesterday shows exactly what that reality looks like:inflation got away from the Fed in 2020, and we haven’t been anywhere near close to returning it toward the baseline trend we have tried to revert to.In fact, the chart shows the delta between the 2% baseline target and current inflation aswidening.

That pressure intensified today after a major upside surprise in wholesale inflation.

The latest producer price index report showed wholesale prices rose 1.4% in April, nearly triple expectations of 0.5% and well above March’s upwardly revised 0.7% increase. On an annual basis, producer prices climbed 6%, marking the biggest increase since December 2022.

This matters because producer prices often serve as an early warning signal for future consumer inflation. Rising input costs eventually work their way through supply chains and show up in prices paid by households. The bigger issue is that this increasingly looks like something broader than a temporary energy spike. Pipeline inflation is building again at a time when the Fed had been hoping for sustained disinflation.

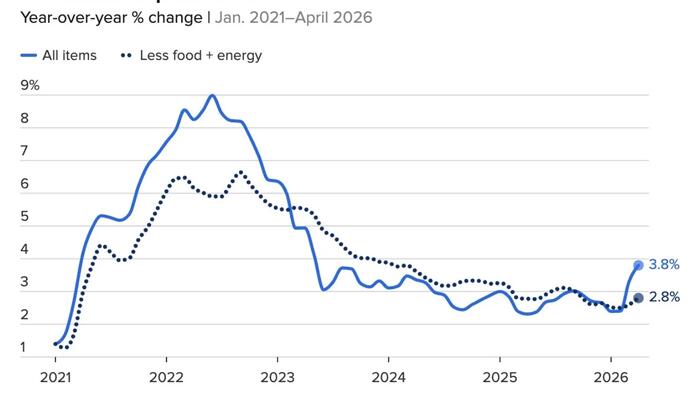

Meanwhile asCNBC noted earlier in the weekthat the CPI was also still coming in hotter than expected — which was already hot at 3.8%. Don’t lose sight of the fact that the Fed’s target is 2%, so this is nearlydoublewhat the Central Bank is gunning for:

Source: ZeroHedge News