As DB's Jim Reid tallies overnight, it has now been 73 days since the war in Iran began, with the past 32 marked by a stalemate characterized by a mix of truce and ongoing ceasefire. The absence of any meaningful kinetic activity for over a month suggests a firm US preference for reaching a deal. However, a counterpoint is that uncertainty over who holds negotiating authority in Iran may be complicating progress and delaying more difficult times ahead. It remains an unusual conflict with little action now for a month. In simple terms though, as long as the Strait of Hormuz stays closed, markets remain on a knife edge.Polymarket currently assigns a 39% probability to it fully reopening by 30 June.

The latest is that oil and yields are up again this morning as President Trump has posted that "I have just read the response from Iran's so called 'Representatives'" which he went on to call "TOTALLY UNACCEPTABLE". This was based on a WSJ report that suggested Iran was offering to transfer some of highly enriched uranium to another country but wouldn't dismantle its nuclear facilities. Iran's official news agency has disputed the report anyway. Brent is up +4.23% and 10yr US yields are up +3.5bps. However, US and European equity futures are largely flat and Asian equities are largely higher on the AI trade. The KOSPI is on fire again with the index up +4.0% as semiconductors surge again. The index has crossed +85% YTD.

This comes ahead of the planned mid-to end week meeting between US President Donald Trump and China’s President Xi Jinping in Beijing. It’ll be interesting to see whether this meeting does anything to shape negotiations in the war. Both leaders would clearly like to show their influence on the world stage. So certainly the biggest headline event of the week(full preview here).

Before that, the new week arrives with markets still processing last Friday’s US payrolls report, which came in broadly firm and reinforced the view that labor market conditions remain resilient. While not strong enough to decisively alter the policy outlook,the release did little to ease concerns that underlying inflation pressures could persist, especially given still-solid wage dynamics. Against this backdrop, outside of the Iran War developments which will of course take center stage, the coming week will remain centered on the US, with a dense run of data and policy developments.

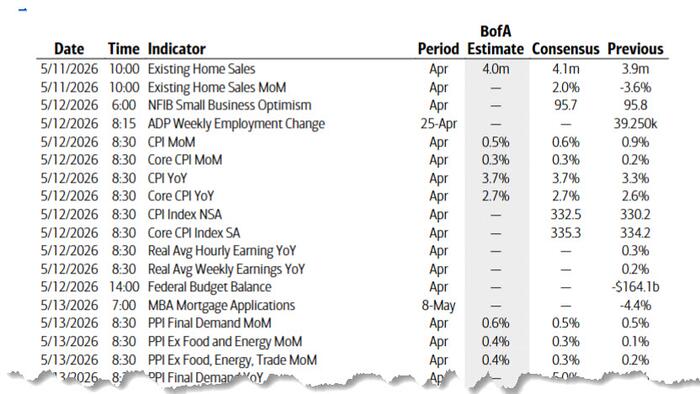

This week's focal point will betomorrow’s April CPI report. DB economists expect headline inflation to rise by +0.58% month-on-month, moderating from March’s +0.9%, but still relatively firm. In contrast, the core measure is projected to accelerate to +0.39% MoM from +0.2%, suggesting underlying price pressures remain sticky even as energy-related effects fade. The YoY rates would move from 3.3% to 3.8% for the former and from 2.6% to 2.8% for the latter.

Producer price datafollows on Wednesday and then the remainder of the week shifts towards activity indicators. DB economists expect retail sales to decline by -0.3% MoM after March’s strong +1.7% increase, pointing to some payback in consumer spending. Meanwhile, industrial production is forecast to rise modestly by +0.2% MoM following a -0.5% drop previously, suggesting a tentative stabilization in manufacturing output.

Policy and politics will also be important.A Senate vote on Kevin Warsh’s nomination as Fed Chair is scheduled for today, just days before Jerome Powell’s term is set to expire at the end of the week.It's possible the vote could get pushed back a day or so due to other Senate business but by the end of the week you would expect Warsh to have taken Miran's seat on the board with Powell staying on the committee.

In Europe,inflation readings from Denmark and Norway today are followed with Germany’s ZEW survey tomorrowwith sentiment darkening even with the nation's extraordinary fiscal package. Later in the week, theECB’s economic bulletinmay offer additional context on the central bank’s assessment of inflation and activity trends.

In the UK, attention will be split between politics and macro. The State Opening of Parliament and the King’s Speech on Wednesday will outline the government’s legislative agenda for the year ahead. With PM Starmer under tremendous pressure following the very poor (but broadly as expected) local election results on Thursdaythere is talk of a leadership challenge as soon as today.Backbench MP Catherine West has said she will stand, which would be a stalking horse nomination. However, many left-wing MPs (as she is) have urged her not to as their preferred candidate Andy Burnham is not currently an MP. They fear an election now might be a bit too early and may allow a more moderate candidate like Wes Streeting to prevail. So timing tactics could prolong Starmer’s reign. A reminder that in September last year, Mr Burnham said that the UK should no longer be “in hock to the bond markets”. This caused a spike in Gilt yields and although he subsequently downplayed the remarks, this is something to watch carefully as we navigate the politics of the next few days and weeks. On the data side, Q1 UK GDP on Thursday will offer up the latest state of play growth wise.

In Asia, Japan’s schedule includes household spending data tomorrow, alongside the Economy Watchers survey and bank lending figures on Wednesday. In addition, the Bank of Japan will publish its summary of opinions from the April meeting, which should provide greater insight into policymakers’ thinking and any emerging shifts in the policy stance.

Source: ZeroHedge News