Authored by Lance Roberts via RealInvestmentAdvice.com,

Last week, we discussed theS&P earnings recordand why such record earnings could be a warning for the market. I want to continue that discussion by focusing not only on what has happened but also on what is expected to happen in the future. While the Q1 2026 earnings results are spectacular, so far, the earnings estimate revisions behind them are the real story.

The first-quarter 2026 earnings season is delivering results that Wall Street rarely sees. With roughly two-thirds of the S&P 500 having reported, the blended growth rate has climbed to 27.1% year-over-year, more than double the 13.2% that consensus modeled at the end of the quarter on March 31. If that figure holds, it will be the strongest year-over-year print since the post-COVID rebound quarter of Q4 2021. 84% of companies have beaten EPS, 81% have beaten revenue, and the average earnings surprise sits at 20.7%, nearly three times the 5-year average of 7.3%.

That’s the surface story. The more interesting question, and the one investors should be asking, iswhyanalysts were so wrong heading in, and what it means that they’re now revising earnings estimates higher with a velocity that has almost no historical parallel.

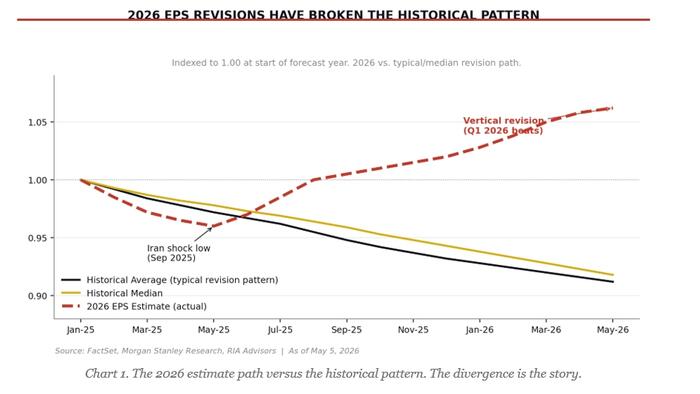

Look at Morgan Stanley’s chart of consensus 2026 earnings estimate revisions versus history. In any normal year, by the time Q1 earnings season rolls around, analysts have been quietly walking earnings estimates down for six months. The historical median revision pattern drifts from 1.00 in January to roughly 0.92 by year-end. Two years of cuts. That’s the analyst playbook. Start the year too optimistic, get reset by reality, and end the year right.

This year is doing the opposite. The 2026 earnings estimate index cratered to 0.96 last summer during the Iran shock, then turned vertical. By May, it’s broken above 1.06. We’re looking at a roughly 14-point swing in earnings estimates relative to the historical pattern. That is what Morgan Stanley calls“fairly unprecedented,”and that’s analyst-speak for something they don’t have a clean comparison for.

The Mag 7 alone moved from a 22.4% expected growth rate at the end of March to a 61% blended print today. Four of the top five contributors to S&P 500 earnings growth this quarter are Alphabet, NVIDIA, Amazon, and Meta. The same four names driving index returns are now driving the earnings estimate revisions. That’s not a coincidence, and there is more to this story as noted by Sage Road Research:

“The AI distortion goes beyond stock prices to profits. Total S&P 500 earnings are on track to rocket 27% higher in the first quarter, FactSet estimates.But profits for the Mag-7 alone will be up 61%; for the other 493, just 16%, a figure itself inflated by semiconductor companies like Micron.This is skewing the division of the economic pie between capital and labor. As profits gallop ahead, labor compensation (wages and benefits) grew just 3.1% annualized in the first quarter, and actually shrank 0.5% after inflation, the Labor Department reported Thursday. Labor’s share of total business-sector output fell to 54.1%, the lowest since records began in 1947.” –@TrevorNoren

So, if it isn’t consumers’ and subsequently economic growth, driving earnings estimate revisions, then what is?

Three things are happening at once, and we have to separate them.

Source: ZeroHedge News