In ourpreview to this morning's Quarterly Refunding Statement, we said that we do not expect major changes and that, at most, the treasury might adjust its statement language to soften the forward guidance on possibly futures increase in coupon auction sizes with one likely change would be dropping “at least”while retaining the expectation for unchanged coupon sizes over“the next several quarters”(recall Deutsche Bank said it expects nominal coupon increases beginning in February 2027).

Overnight, JPMorgan agreed, writing that while the current auction calendar will leave Treasury well financed through FY27, "we do not think it will be adequate to meet the widening funding gap from FY27 and onward, and we continue to project a series of coupon auction increases beginning in February 2027." Accordingly, like DB, JPM alsoexpected the Treasury to remove “at least” from the statement that “Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters."The bank said that If its expectations are realized, "we think this could push intermediate yields higher."

Well, moments ago the Treasury published its latest Quarterly Refunding Announcement, and contrary to prevailing expectations, it refused to make even a gentle hint at rising coupon sizes by keeping the "at least" language from the abovementioned statement, instead keeping it as is, or rather as was:

Based on current projected borrowing needs, Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters

In other words, the US Treasury signaled again that it’s still comfortable using Yellen'sActivist Treasury Issuanceplaybook to issue Bills, and not increase coupon issuance, to meet escalating government borrowing needs, even as warnings emerge about the strategy’s risks.

Ahead of the QRA,dealers were divided heading into the so-called quarterly refunding release on whether it might alter its guidance.Outsize US fiscal deficits make an expansion in longer-dated auctions practically inevitable at some stage. The department on Monday boosted its estimate for net borrowing this quarter amid lower net cash flows.

US debt managers have been using the same forward guidance since early 2024, in a policy that’s steadily boosted the share of bills of total debt outstanding (to roughly 22% from 14% before covid). The International Monetary Fund cautioned last month that this leaves federal debt costs more vulnerable to sudden swings in rates and shifts in sentiment, because auctions are more frequent.

And sure enough, with no changes to the forward guidance:

The rest of the statement was also in line with expectations, with the Treasury stating "it believes its current auction sizes leave it well positioned to address potential changes to the fiscal outlook and to the size and composition of the SOMA portfolio." It added that it was monitoring SOMA purchases of Treasury bills and growing demand for Treasury bills from the private sector. And, as before, looking ahead the treasury continues to evaluate potential future increases to nominal coupon and FRN auction sizes, with a focus on trends in structural demand and potential costs and risks of various issuance profiles.

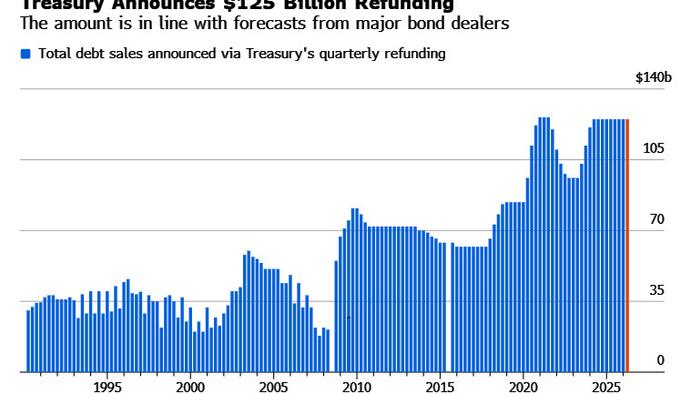

Looking at the actual refunding auctions next, theTreasury’s refunding debt sales will total $125 billion, unchanged from the sum unveiled in February and in line with the expectations of Wall Street bond dealers.

Source: ZeroHedge News